An article by

Wise Soo-Penning

Published on

30/04/2026

Updated on

08/05/2026

Reading time

3 min

Payment as a Sovereign Task

Four central fields of action

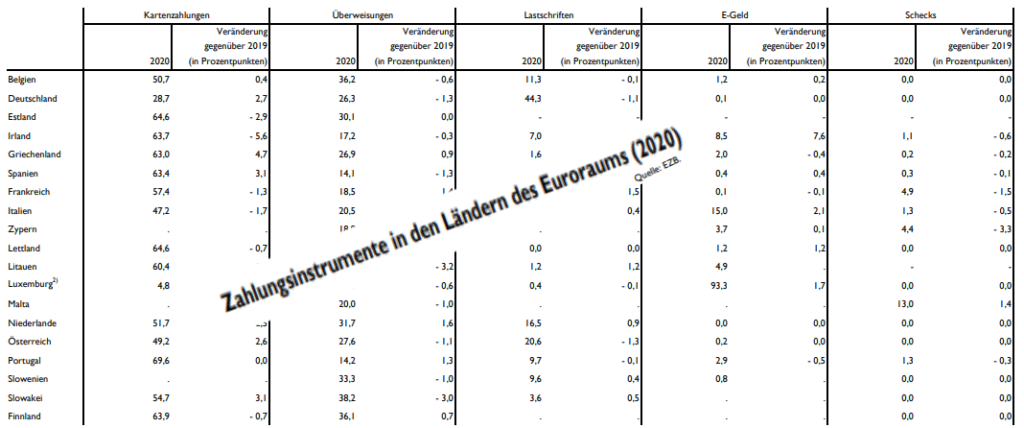

The digital euro for everyday life (Retail Payments)

The digital euro for everyday life (Retail Payments)

The European retail market is highly fragmented, and many countries rely heavily on non-European providers for digital payments. With the digital euro project, the Eurosystem is bringing central bank money into the digital age. The digital euro is intended to become a Europe-wide, secure, and free payment solution for everyday use. It protects users’ privacy, promotes financial inclusion, and makes Europe less dependent on international corporations. Additionally, resilience is increased, as the digital euro also enables offline payments. A possible introduction is targeted for the year 2029.

Tokenization and large-value payments (Wholesale Payments)

Tokenization and large-value payments (Wholesale Payments)

In large-value payment transactions between financial institutions, distributed ledger technology (DLT) is driving profound changes. Through initiatives such as Pontes and Appia the Eurosystem is developing solutions to settle tokenized payments and securities transactions securely in central bank money. Central bank money remains the safe, indispensable anchor of the two-tier monetary system in order to maintain financial stability. This system is to be complemented by highly regulated private digital assets such as tokenized deposits and European stablecoins. At the same time, the existing real-time gross settlement system T2 (formerly TARGET) continues to be strengthened as the backbone of the system.

An efficiency boost for corporate payments (B2B)

An efficiency boost for corporate payments (B2B)

Für die europäische Wirtschaft sind reibungslose Business-to-Business (B2B)-Zahlungen essenziell. Der Schwerpunkt liegt hier auf Standardisierung und Automatisierung. Die Umstellung auf den globalen Nachrichtenstandard ISO 20022 hilft dabei, Zahlungsdaten verlustfrei zu übermitteln und Prozesse ohne manuelle Eingriffe zu automatisieren. Zudem bietet das Eurosystem mit dem TIPS-System eine Infrastruktur, die Echtzeitzahlungen an 365 Tagen im Jahr rund um die Uhr in Sekunden abwickelt.

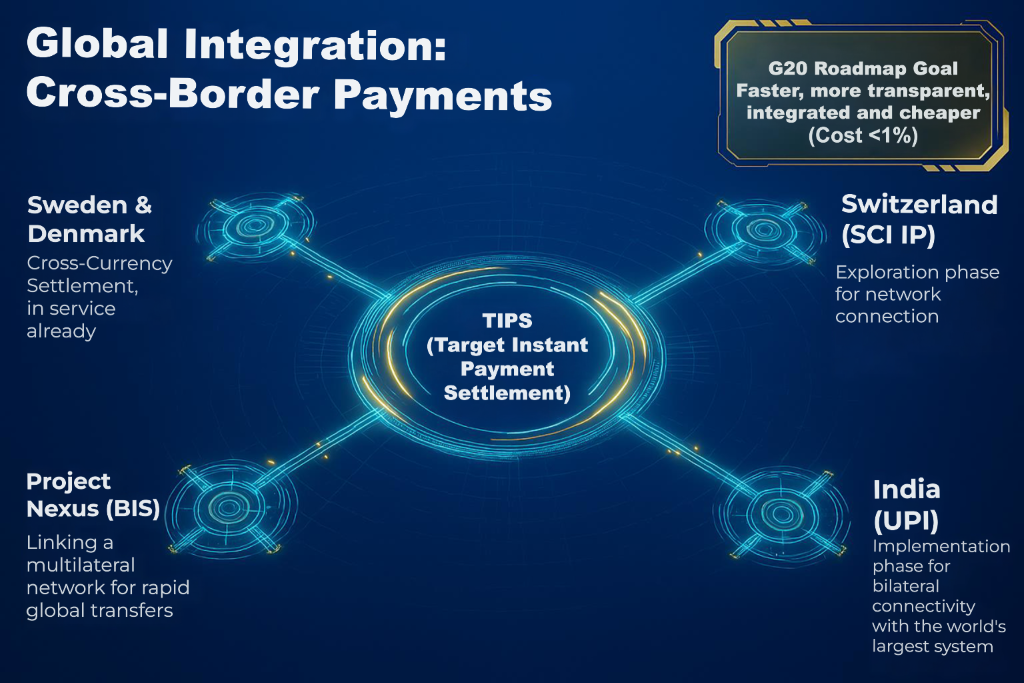

Pay cheaper worldwide (Cross-Border Payments)

International payments beyond the EU borders are still often too expensive, opaque, and slow. The Eurosystem therefore actively supports the G20 roadmap to improve cross-border payments. A central project is the international networking of the European TIPS system. Through partnerships with real-time payment systems in Switzerland or the Indian Unified Payments Interface (UPI), global money transfers are intended to become significantly faster and cheaper in the future.

Conclusion

Share